Memory Chip Market Insights: Chip Miniaturization, Performance Optimization & Forecast to 2034

How semiconductor miniaturization, advanced fabrication techniques, and chip stacking technologies are enhancing performance while reducing power consumption in modern memory chip designs

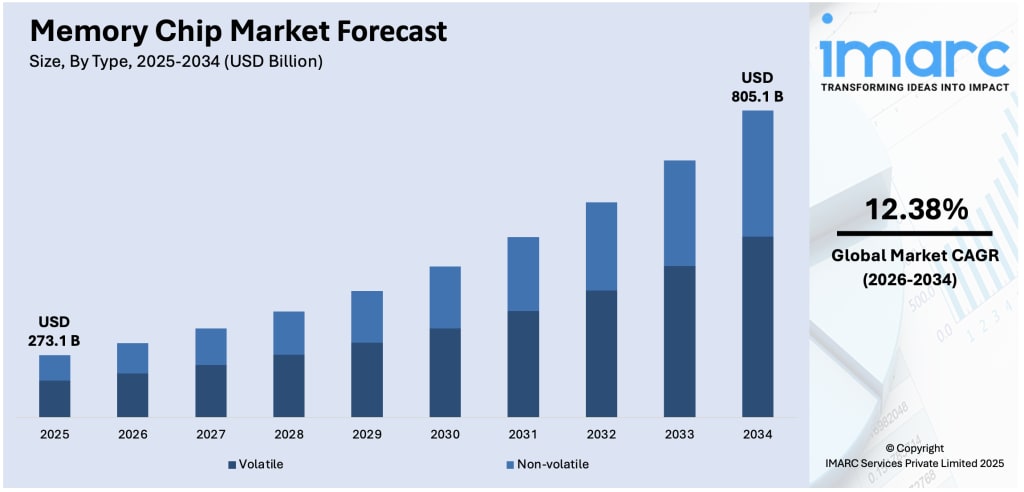

The memory chip sector has evolved into a cornerstone of the modern digital economy, moving far beyond its traditional role in personal computing. Today, it serves as the fundamental engine for artificial intelligence (AI), high-performance computing, and the massive data centers that power our global infrastructure. According to IMARC Group’s latest data, the global memory chip market size was valued at USD 273.1 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 805.1 Billion by 2034, exhibiting a CAGR of 12.38% from 2026-2034.

The industry is currently navigating a structural shift, where demand is increasingly dictated by industrial-scale AI builds rather than just consumer upgrade cycles. As hyperscale cloud providers commit hundreds of billions to infrastructure, the need for high-bandwidth and high-density memory has created a unique "supercycle" environment. Modern memory solutions ranging from 3D NAND to advanced DRAM are being redesigned for greater power efficiency and faster data transfer to meet the rigorous demands of machine learning and autonomous systems. With the market projected to nearly triple in value over the next decade, the focus has shifted toward securing supply chains and innovating in vertical stacking technologies to overcome physical space constraints in high-performance hardware.

Memory Chip Market Growth Drivers:

- Explosion of Generative AI and Data Center Expansion

The rapid integration of Large Language Models (LLMs) and generative AI across industries is fundamentally altering memory requirements. Unlike traditional computing, AI training and inference demand massive amounts of High Bandwidth Memory (HBM) to process complex datasets in real-time. Cloud giants like Microsoft, Meta, and Google are projected to invest roughly USD 650 billion in data center infrastructure in 2026 alone. This industrial-scale buildout requires specialized memory clusters that offer 50% more capacity than previous generations, ensuring that hardware can keep pace with the 25-fold projected growth of the global AI sector.

- Rising Complexity in Automotive Electronics and ADAS

Modern vehicles are transforming into "computers on wheels," requiring sophisticated memory for Advanced Driver-Assistance Systems (ADAS) and in-vehicle infotainment. Level 3 and Level 4 autonomous driving platforms generate terabytes of data that must be stored and processed instantly for safety-critical decisions. Memory manufacturers are responding by developing automotive-grade chips, such as eMRAM, designed to operate reliably at extreme temperatures. With the average semiconductor cost per vehicle rising as the industry pivots toward Electric Vehicles (EVs), memory chips have become essential for managing everything from battery efficiency to high-definition sensor mapping.

Grab Your Free "Memory Chip Market" Trends & Forecast Sample Report

- Steady Demand for High-Performance Consumer Gadgets

While AI dominates the headlines, the sheer volume of smartphones, laptops, and tablets remains a primary engine for the market. Global smartphone shipments reached approximately 1.24 billion units recently, with consumers increasingly opting for premium devices that support 5G and on-device AI features. These advanced functionalities require higher-density DRAM and faster NAND flash storage to enable seamless multitasking and high-resolution media handling. In 2025, the Laptop and PC segment alone accounted for 45.2% of the market share, driven by a continuous refresh cycle for high-performance machines capable of supporting remote work and gaming.

Memory Chip Market Trends:

- Shift Toward 3D NAND and Vertical Stacking Architectures

To overcome the physical limits of traditional 2D memory, the industry has pivoted toward 3D NAND technology. This approach stacks memory cells vertically in multiple layers—often exceeding 200 to 232 layers in the latest high-end SSDs—to maximize storage density without increasing the chip's footprint. This transition significantly improves cost efficiency per bit and reduces power consumption, which is critical for mobile devices and green data centers. Leading manufacturers are now competing to increase layer counts further, with 3D architectures becoming the standard for enterprise-grade storage and high-capacity consumer electronics.

- Dominance of High Bandwidth Memory (HBM) in

AI Accelerators A defining trend in the current "supercycle" is the meteoric rise of High Bandwidth Memory, specifically HBM3E and the emerging HBM4. These chips are essential for AI GPUs, providing the "pipes" necessary for data to flow rapidly between storage and processing units. HBM is expected to account for roughly 25% of total DRAM wafer production by 2026. Because producing HBM is more complex and occupies more manufacturing capacity than standard DRAM, it has led to a market environment where high-end memory is often sold out a year in advance, secured by multi-year agreements with major AI developers.

- Nationalization of Semiconductor Supply Chains

Geopolitical tensions and the strategic importance of "silicon sovereignty" are driving governments to invest heavily in domestic chip production. Through programs like the U.S. CHIPS Act and similar initiatives in Europe and Japan, billions in subsidies are being funneled into building new fabrication facilities. This trend aims to reduce reliance on concentrated manufacturing hubs in Asia and create more resilient, localized supply chains. For example, investment consortiums are now targeting trillions in funding for semiconductor infrastructure to ensure that critical industries from defense to healthcare have a guaranteed supply of advanced memory components.

Recent News and Developments in Memory Chip Market

- March 2026: The U.S. government announced an expansion of its "Pax Silica" program, aiming to facilitate a voluntary investment consortium targeting USD 4 trillion for semiconductor supply chains and critical minerals to secure AI chipmaking for the U.S. and its allies.

- February 2026: Micron Technology reported a record-breaking quarter, with shares surging over 340% in a twelve-month period, highlighting the massive "disconnect" where AI-driven demand for memory is vastly outstripping the available manufacturing supply.

- January 2026: Samsung Electronics officially signaled the discontinuation of its legacy MLC NAND Flash products, with final deliveries expected this year, as the company reallocates its manufacturing capacity toward higher-density 3D NAND and AI-specific memory.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About the Creator

Andrew Sullivan

Hello, I’m Andrew Sullivan. I have over 9+ years of experience as a market research specialist.

Keep reading

More stories from Andrew Sullivan and writers in Futurism and other communities.

Emotion Detection and Recognition Market Trends: Ethical AI, Privacy Regulations & Industry Forecast to 2034

The global emotion detection and recognition (EDR) market is witnessing a significant transformation as businesses and government agencies increasingly integrate affective computing to create more responsive, human-centric digital environments. Driven by breakthroughs in multimodal AI and the proliferation of biometric-enabled wearables, EDR technology is moving beyond simple facial analysis to comprehensive emotional intelligence. According to IMARC Group’s latest data, the global emotion detection and recognition market size was valued at USD 64.9 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 243.7 Billion by 2034, exhibiting a CAGR of 15.37% from 2026-2034.

By Andrew Sullivana day ago in Futurism

How machines can learn from human behaviour

In order to understand where we are and where we are going, we need to understand where we were first. - Susan Fourtane Could a human behaviour simulator be embedded into a robot or online avatar to the point that it’s hard to distinguish between a real person or artificial intelligence? Scientists have been upping the stakes in this “Turing test” for years, to the point that human-mimicking programmes are ready to answer tricky questions, assist people with online shopping or be companions.

By Susan Fourtané 9 days ago in Futurism

Chronic Ache in the Soul of a Single Parent

There is a chronic ache in the soul of a single parent. It lingers, feeling endless. This ache feels so difficult, especially when you look at other families. They seem so… whole. They seem so joyful and complete. There is a husband and a wife and children in a stroller. Thinking about your single state, you realize how awkward you feel, how out of place at various functions and gatherings. They are all happily together and you’re miserably alone. Disappointment with the current life circumstances just settles in to stay, or so it feels. How could these layers of disappointment be broken up anyhow?

By Rowan Finley 7 days ago in Humans

Comments

There are no comments for this story

Be the first to respond and start the conversation.